The generally light-touch regulatory approach to America’s Internet industry has been a big success story. Broadband, wireless, digital devices, Internet content and apps — these technology sectors have exploded over the last half-dozen years, even through the Great Recession.

So why are Washington regulators gradually encroaching on the Net’s every nook and cranny? Perhaps the explanation is a paraphrased line about Washington’s upside-down ways: If it fails, subsidize it. If it succeeds, tax it. And if it succeeds wildly, regulate it.

Whatever the reason, we should watch out and speak up, lest D.C. do-gooders slow the growth of our most dynamic economic engine.

Last December, the FCC imposed a watered down version of Net Neutrality. A few weeks ago the FCC asserted authority to regulate prices and terms in the data roaming market for mobile phones. There are endless Washington proposals to regulate digital advertising markets and impose strict new rules to (supposedly) protect consumer privacy. The latest new idea (but surely not the last) is to regulate prices and terms of “special access,” or Internet connectivity in the middle of the network.

Special access refers to high-speed links that connect, say, cell phone towers to the larger network, or an office building to a metro fiber ring. Another common name for these network links is “backhaul.” Washington lobbyists have for years been trying to get the FCC to dictate terms in this market, without success. But now, as part of the proposed AT&T-T-Mobile merger, they are pushing harder than ever to incorporate regulation of these high-speed Internet lines into the government’s prospective approval of the acquisition.

As the chief opponent of the merger, Sprint especially is lobbying for the new regulations. Sprint claims that just a few companies control most the available backhaul links to its cell phone towers and wants the FCC to set rates and terms for its backhaul leases. But from the available information, it’s clear that many companies — not just Verizon and AT&T — provide these Special Access backhaul services. It’s not clear why an AT&T-T-Mobile combination should have a big effect on the market, nor why the FCC should use the event to regulate a well-functioning market.

Sprint is a majority owner and major partner of 4G mobile network Clearwire, which uses its own microwave wireless links for 90% of its backhaul capacity. Sprint used Clearwire backhaul for its Xohm Wi-Max network beginning in 2008 and will pay Clearwire around a billion dollars over the next two years to lease backhaul capacity.

T-Mobile, meanwhile, uses mostly non-AT&T, non-Verizon backhaul for its towers. Recent estimates say something like 80% of T-Mobile sites are linked by smaller Special Access providers like Bright House, FiberNet, Zayo Bandwidth, and IP Networks. Lots of other providers exist, from the large cable companies like Comcast, Cox, and TimeWarner to smaller specialty firms like FiberTower and TowerCloud to large backbone providers like Level 3. The cable companies all report fast growing cell site backhaul sales, accounting for large shares of their wholesale revenue.

One of the rationales for AT&T’s purchase of T-Mobile was that the two companies’ cell sites are complementary, not duplicative, meaning AT&T may not have links to many or most of T-Mobile’s sites. So at least in the short term it’s likely the T-Mobile cells will continue to use their existing backhaul providers, who are, again, mostly not Verizon or AT&T. It’s possible over time AT&T would expand its network and use its own links to serve the sites, but the backhaul business by then will only be more competitive than today.

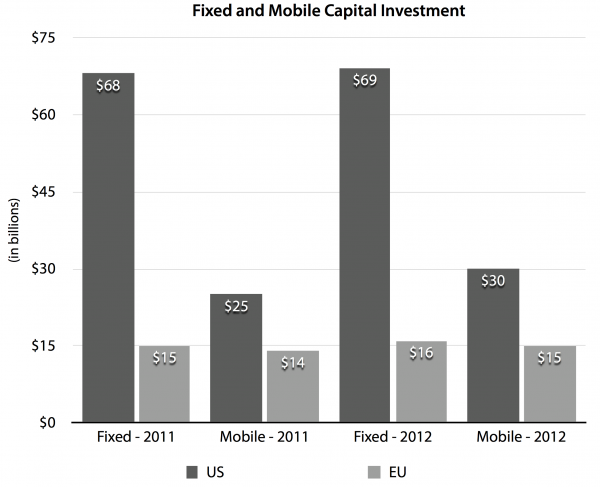

This is a mostly unseen part of the Internet. Few of us every think about Special Access or Backhaul when we fire up our Blackberry, Android, or iPhone. But these lines are key components in mobile ecosystem, essential to delivering the voices and bits to and from our phones, tablets, and laptops. The wireless industry, moreover, is in the midst of a massive upgrade of its backhaul lines to accommodate first 3G and now 4G networks that will carry ever richer multimedia content. This means replacing the old T-1 and T-3 copper phone lines with new fiber optic lines and high-speed radio links. These are big investments in a very competitive market.

Given the Internet industry’s overwhelming contribution to the U.S. economy — not just as an innovative platform but as a leading investor in the capital base of the nation — one might think we wouldn’t lightly trifle with success. The chart below, compiled by economist Michael Mandel, shows that the top two — and three out of the top seven — domestic investors are communications companies. These are huge sums of money supporting hundreds of thousands of jobs directly and many millions indirectly.

via Michael Mandel

We’ve seen the damage micromanagement can cause — in the communications sector no less. The type of regulation of prices and terms on infrastructure leases now proposed for Special Access was, in my view, a key to the 2000 tech/telecom crash. FCC intrusions (remember line sharing, TELRIC, and UNE-P, etc.) discouraged investments in the first generation of broadband. We fell behind nations like Korea. Over the last half-dozen years, however, we righted our communications ship and leapt to the top of the world in broadband and especially mobile services.

I’m not arguing these regulations would crash the sector. But the accumulated costs of these creeping Washington intrusions could disrupt the crucial price mechanisms and investment incentives that are no where more important than the fastest growing, most dynamic markets, like mobile networks.Time for FCC lawyers to hit the beach — for Memorial Day weekend . . . and beyond. They should sit back and enjoy the stupendous success of the sector they oversee. The market is working.

— Bret Swanson